Updated on

Selling a company is rarely just a financial decision for an Italian founder. It is the transition from “founder” identity to “former founder” — a transformation that the technical M&A playbook does not capture. This guide approaches business sale from the founder’s perspective: the human, identity, and family dimensions alongside the operational and financial framework. It is the complement to standard M&A guides — what founders specifically need to understand before initiating a sale process.

Key takeaways

- For Italian founders, business sale is identity transition first, financial transaction second — the technical playbook addresses only half the journey.

- Personal motivations (succession, age, life-stage change) and strategic motivations (market timing, consolidation) typically converge in the optimal sale window.

- Structured 4-phase sale process: preparation, buyer search, negotiation and DD, closing and post-closing — 6-12 months typical duration.

- Valuation methods triangulate DCF, market multiples, transaction comparables — no single method is sufficient.

- The founder’s emotional readiness materially affects deal outcomes — psychological preparation matters as much as financial preparation.

Why and when to sell a company: strategic motivations

Personal and family motivations

For Italian founders, personal motivations often drive timing more than market dynamics: (a) age and retirement planning, (b) health considerations affecting strategic capacity, (c) family-business succession not feasible (children not interested or not suitable), (d) desire to diversify wealth away from concentrated business asset, (e) life-stage change requiring new project. These motivations are often the deepest driver behind a sale decision — and the most underestimated in technical M&A literature.

Strategic and market motivations

Market motivations: industry consolidation creating active buyer competition, sector-specific premium valuations, regulatory environment favouring exit timing, competitive intensification making sale of better business than continued solo struggle. Pattern: founders sell at peaks when market and personal motivations converge — selling reluctantly during decline phase destroys 25-40% of achievable value.

Understanding the perfect “timing” for sale

Optimal timing combines five factors: company in growth phase with visible 18-24 months runway, sector in consolidation with active buyer competition, macro environment supportive (rates allow buyer leverage), founder in psychologically prepared phase, family alignment on sale decision. Critical — psychological readiness is equally important to financial readiness. Founders who sell while ambivalent often regret decision or sabotage negotiation through unconscious resistance.

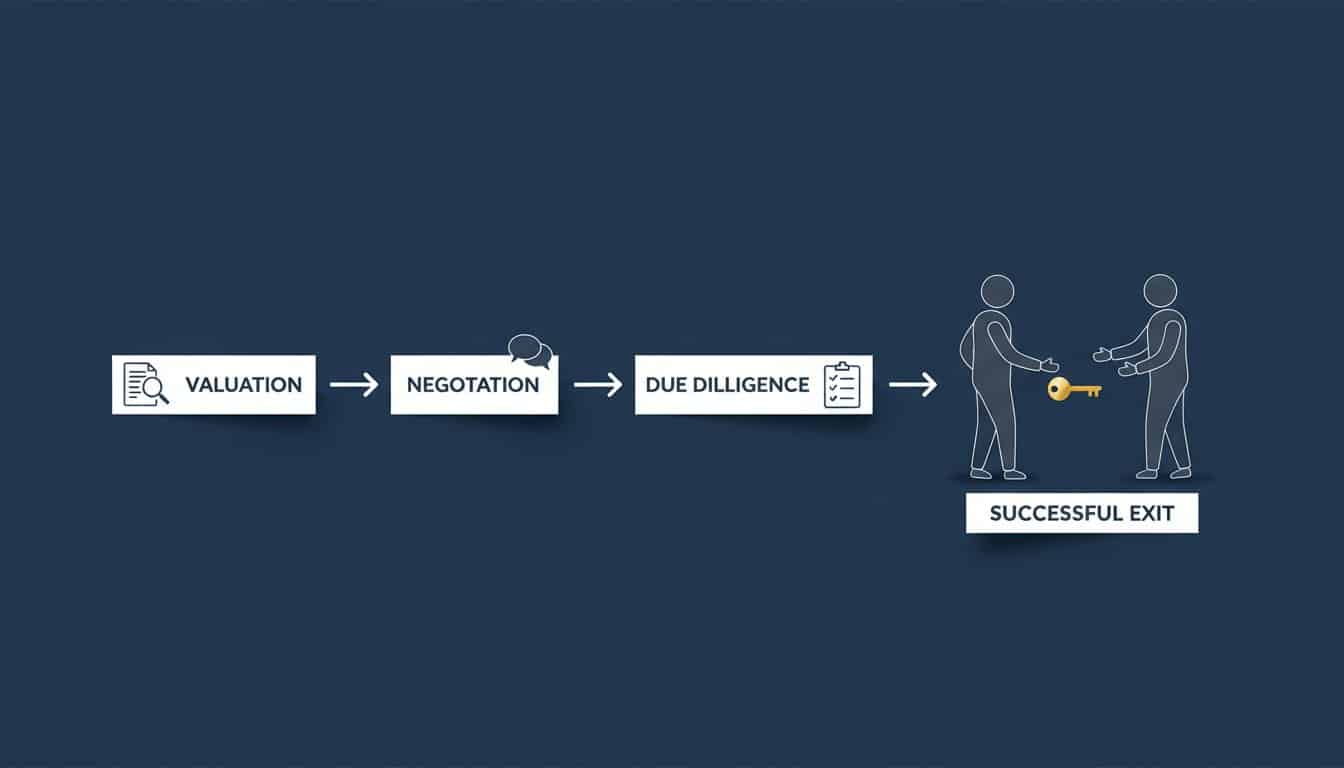

The business sale process explained step by step

Phase 1: preparation and company valuation

2-4 months. Independent valuation, operational normalisation (clean accounting, audited financials, normalised personal-corporate boundaries), legal due diligence (clean structure, no pending disputes), data room preparation, advisor team selection. Critical: address structural issues before sale process begins.

Phase 2: buyer search and confidential marketing

2-3 months. Information Memorandum and anonymous teaser preparation, buyer mapping (25-40 candidates), bilateral NDAs (15-20), distribution to interested buyers, non-binding offers from 8-12 buyers, finalist selection.

Phase 3: negotiation and due diligence

2-3 months. Full data room access, comprehensive DD (financial, legal, tax, commercial), SPA negotiation. This is the phase where founder emotional management matters most: buyer DD often surfaces issues that founders had not consciously acknowledged. Senior advisor support during this phase prevents emotional decisions destroying deal value.

Phase 4: closing and post-closing

1-3 months. Conditions precedent, signing, payment and ownership transfer, post-closing transition. Critical for founder: structured handover with continued involvement period (12-36 months typically), gradual identity transition from operational leader to advisor role.

How is company value determined? The valuation methods

Asset methods: tangible value

Net asset value, adjusted book value, replacement cost methods. Useful as floor reference; not capturing intangibles (brand, customer relationships, know-how, growth potential). Pattern: asset methods typically 30-60% below market value for going concerns; appropriate for liquidation scenarios only.

Income and financial methods (DCF): future value

DCF projects future cash flows discounted at appropriate WACC. Foundation method capturing forward-looking value. Limitation: depends heavily on forecast assumptions. Italian mid-market WACC typically 10-14% reflecting market and country risk premiums.

Market methods (multiples and transaction comps)

EV/EBITDA, EV/Revenue, P/E multiples of comparable listed peers or recent M&A transactions. Provides market validation. Italian mid-market discount: 15-30% vs US/UK equivalents. Triangulation with DCF and asset methods provides robust valuation range.

The founder’s identity dimension: what M&A playbooks miss

For Italian founders, business is often objectified biography — selling means transitioning identity. Recognised dimensions: (a) Continuity preservation — buyer willing to preserve business name, location, key team, (b) Founder legacy — recognition of founder’s contribution beyond financial valuation, (c) Stakeholder impact — employees, suppliers, community considerations, (d) Transition support — structured post-closing involvement vs clean break preference. Best M&A advisors address these dimensions explicitly; technical playbooks ignore them. Founders feeling their identity respected by buyer typically close deals 15-25% above multiples; founders feeling disrespected often kill deals at full multiples.

Frequently asked questions

How psychologically prepared should I be before initiating sale process?

Critical readiness check: can you describe your post-sale 5-year plan? If yes — psychologically ready. If no — pause for clarity before initiating process. Founders without post-sale vision often sabotage negotiation unconsciously.

Should I tell employees and customers about potential sale?

No, not during sale process. Confidentiality essential — premature disclosure destabilises operations and reduces buyer perception of seller commitment. Disclosure occurs at SPA signing or closing, depending on deal specifics.

How do I handle children who work in the business?

Critical pre-process conversation: clarify their post-sale role expectations. Options: continued employment in new ownership (if buyer values), exit with compensation package, new venture funded by sale proceeds. Pattern: family alignment on sale decision essential — without it, founders often sabotage process.

Can I structure earn-out tied to my continued involvement?

Yes, common pattern. 60-80% cash at closing + 20-40% earn-out over 24-36 months tied to performance metrics with founder continued involvement. Earn-out becomes incentive for smooth transition. Critical: align earn-out metrics with founder’s actual influence post-closing.

What if I change my mind during the process?

Possible until binding LOI signature, costly after. Pre-LOI: 100-200k professional fees lost (advisor, legal, valuation). Post-LOI: termination fees + reputational damage to founder for future deal attempts. Pattern: founders unsure should not initiate process; clarity precedes action.

Considering selling your business?

30-minute discovery call in confidential setting to discuss your situation — financial, strategic, and identity dimensions integrated. Confidential conversation →

{kind=link}

{kind=link}

{kind=link}