Updated on

The buyout is one of the most strategic and sophisticated extraordinary finance operations. Through leveraged buyout (LBO), management buyout (MBO), management buy-in (MBI), or hybrid structures (BIMBO), buyouts enable acquisition of established businesses through structured debt-equity combinations. This guide explains the operational framework: typologies, strategic objectives, process phases, risks, advisor role.

Key takeaways

- Buyout is acquisition of a company through structured debt-equity combination, typically with leveraged finance enabling lower equity contribution.

- Main typologies: LBO (financial investor-led), MBO (current management acquires), MBI (external management acquires), BIMBO (hybrid internal + external management).

- Strategic objectives: liquidity for seller, continuity for business, growth capital for management, value creation for financial investor.

- Process phases: target identification, structuring, due diligence, financing, closing, post-acquisition value creation.

- Italian mid-market: 100-200 buyout operations per year in EUR 5-200M range, dominant pattern in family business succession.

What a buyout is: fundamental principles of acquisition

The concept of leverage

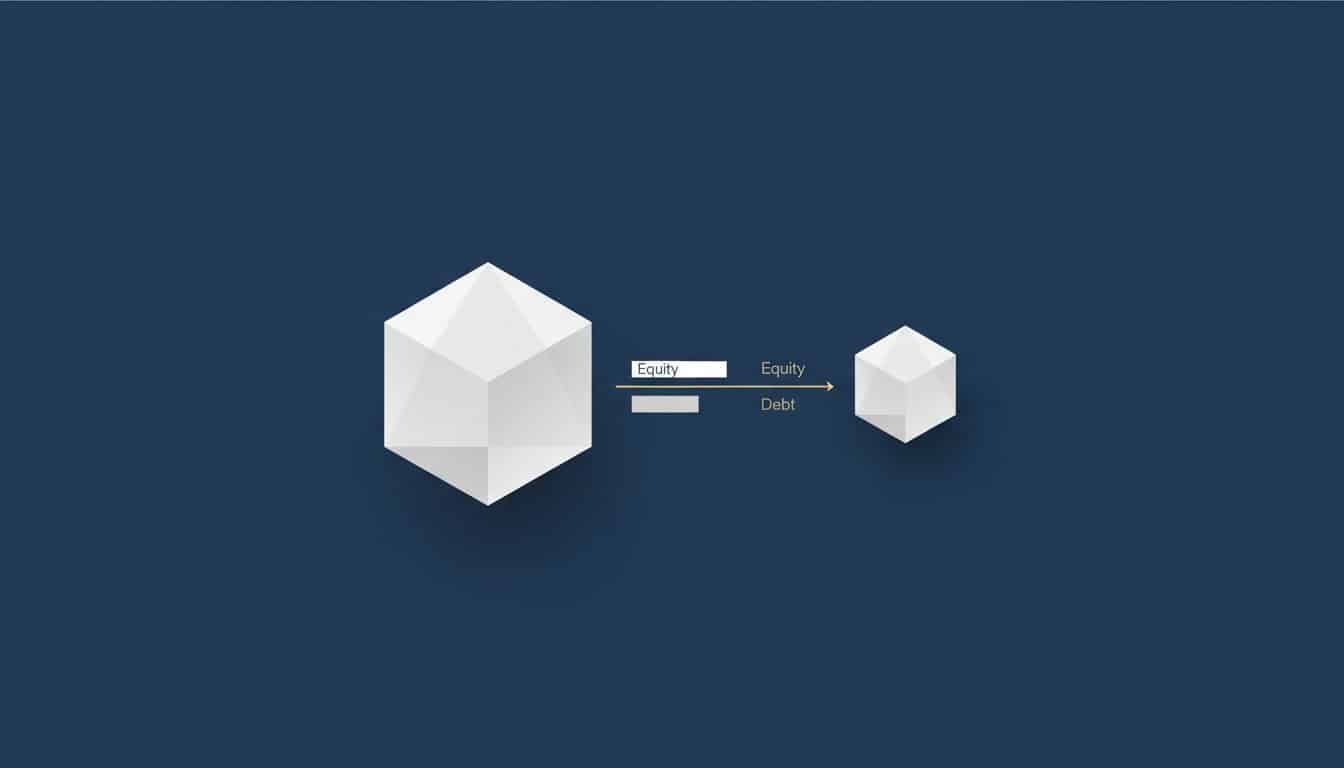

Buyout structures combine equity (typically 30-50% of acquisition price) with debt (50-70%) to acquire target. Leverage amplifies returns on equity but increases financial risk: typical structure uses senior secured debt (3-4x EBITDA), mezzanine debt (1-2x EBITDA), equity (1-2x EBITDA). Pattern: Italian mid-market buyout typically 50-60% debt, 40-50% equity — lower than US/UK due to more conservative banking practices and lower transparent debt markets.

Actors involved in a buyout

- Target: the company being acquired

- Seller: existing owner (founder, family, previous PE)

- Equity sponsor: PE fund or strategic investor providing equity

- Management: existing or new management taking equity participation

- Senior lender: bank providing senior secured debt

- Mezzanine investor: providing subordinated debt (if needed)

- Advisor team: M&A advisor, legal counsel, tax advisor, accounting/audit

Main buyout typologies: LBO, MBO, MBI, BIMBO

Leveraged Buyout (LBO): financial investor-led operation

LBO: PE fund acquires target with leverage, typically planning 4-7 year hold with operational improvements and exit at higher multiple. Italian mid-market: typical PE buyout at 7-10x EBITDA, target IRR 18-25%. Sources of returns: EBITDA growth (50% of value creation), multiple expansion (25%), debt paydown (25%).

Management Buyout (MBO): when managers become entrepreneurs

MBO: existing management acquires the company, typically with PE backing as equity sponsor. Pattern: management contributes 5-15% of equity (often through new bank loans secured by management’s personal assets), PE provides 35-45%, debt 50%. Advantages: management continuity preserved, founder transition smoother, operational risks minimised. Italian mid-market: MBO common in family business succession where children unwilling but management willing.

Management Buy-in (MBI) and BIMBO

MBI: external management team acquires target, typically with PE backing. Higher risk than MBO (no incumbent management knowledge) but useful when existing management not suitable. BIMBO (Buy-In Management Buyout): hybrid of existing management + external management, often combining sector knowledge + new growth perspective. Pattern: BIMBO increasingly common 2022-2025 for businesses requiring both continuity and transformation.

Strategic objectives of the buyout: why and when it makes sense

Advantages for the entrepreneur or selling owner

- Liquidity at favourable multiples (typically 1-2x premium vs trade sale)

- Continuity preservation (management continues, employees retained, brand preserved)

- Smooth transition with structured handover

- Possible retained minority (typically 10-20%) for upside participation

- Reduced disruption vs strategic sale

Advantages for buyers (management or Private Equity)

- Equity participation in established business with proven cash flows

- Leverage amplifies returns on equity (target 18-25% IRR)

- Operational improvement potential (cost optimisation, growth acceleration)

- Sector specialisation building (PE) or wealth creation (management)

- Multiple expansion through operational improvement (typical 1-2x EBITDA multiple uplift)

Phases and risks of a buyout operation: the advisor’s role

Key phases of the buyout process

- Target identification and approach: PE sponsor identifies target, initial confidential discussions

- Preliminary structuring: equity-debt structure design, financing strategy

- Due diligence: financial, commercial, operational, legal — 2-4 months

- Final structuring and negotiation: SPA negotiation, financing commitment, equity allocation

- Closing and financing drawdown: signing, debt drawdown, equity injection

- Post-acquisition value creation: 100-day plan, operational improvements, growth acceleration

Risks to evaluate and mitigate

- Leverage risk: high debt makes target vulnerable to operational shocks

- Integration risk: management transition periods can destabilise operations

- Sector cyclicality: leveraged structures exposed to industry downturns

- Refinancing risk: senior debt typically refinanced post-3-5 years; market conditions affect refinancing terms

- Exit timing risk: market conditions at exit affect multiple realisation

Why rely on an expert advisor

Buyout structuring requires multi-disciplinary expertise: financial (debt-equity optimisation), operational (post-acquisition value creation), strategic (target identification, exit planning), legal (SPA negotiation, regulatory compliance). Senior advisor brings integrated capability + network (PE funds, debt providers, management talent). Pattern: advisor fee 1.5-3% of deal value, justified by deal completion + value creation.

Italian buyout market: 2024-2025 specifics

Italian mid-market buyout activity 2024-2025: 100-200 operations per year in EUR 5-200M range. Dominant pattern: family business succession through MBO/BIMBO structures. PE funds active: Italian (Investindustrial, FSI, Clessidra, Charterhouse Italy), international with Italian operations (Bain Capital, CVC, Cinven, EQT). Sector focus: industrial manufacturing, healthcare, consumer brands, tech-enabled services. Average deal multiples: 7-11x EBITDA for premium mid-market businesses.

Frequently asked questions

What is the difference between buyout and acquisition?

Acquisition is general term for buying a company. Buyout specifies the structure: typically leveraged (debt-equity combination), often with management participation. All buyouts are acquisitions; not all acquisitions are buyouts (strategic acquisitions are typically all-equity by industrial buyer).

How much equity does management typically contribute in MBO?

Italian mid-market pattern: 5-15% of total equity. Management contribution often funded through new bank loans secured by management’s personal assets, or through deferred compensation reinvested. Higher contributions (above 20%) signal strong management commitment but require significant personal financial risk.

How is the equity sponsor selected in MBO?

Through structured process: management identifies preferred sponsor types (sector specialist vs generalist, operational vs financial, large vs small fund), advisor approaches 8-12 PE funds with sector match, term sheet negotiation with 2-3 finalists. Critical: select sponsor with values alignment and post-closing collaborative approach.

What is the typical PE hold period in buyouts?

4-7 years for Italian mid-market. Exit options: secondary buyout (sale to another PE), trade sale to strategic acquirer, IPO (rare for mid-market). Pattern: secondary buyout most common 50%+ of exits, trade sale 30-40%, IPO 10% or less.

Can family business be acquired through MBO without losing family character?

Partially. Operational character can be preserved through continued management and culture; ownership character inevitably changes. Pattern: families often retain 10-20% minority post-MBO, preserving family link to business while monetising majority. PE sponsor adapts to family business culture if strong post-closing operational results.

Considering a buyout structure?

30-minute discovery call to discuss your specific situation — seller, management, or PE sponsor — and assess optimal buyout structure. Confidential conversation →

{kind=link}

{kind=link}

{kind=link}